May 1, 2024

Understanding key metrics is essential for making informed decisions regarding real estate investing. One such metric that every investor should be familiar with is the Capitalization Rate or Cap Rate for short. In this article, we will delve into the ins and outs of the Cap Rate and explore why it is considered to be the go-to metric for evaluating the profitability of a real estate investment.

Whether you’re a seasoned real estate investor or just starting, understanding the Cap Rate is crucial. By grasping this key metric, you’ll be better equipped to evaluate potential investment opportunities and achieve your financial goals.

What is The Cap Rate, and Why Is It Important?

The Cap Rate, expressed as a percentage, measures the potential return on investment of a property. It is calculated by dividing the property’s net operating income (NOI) by its current market value. A high Cap Rate indicates a potentially lucrative investment, while a low Cap Rate suggests a property with lower earning potential. Knowing the Cap Rate allows investors to determine how much income an investment property will generate relative to its purchase price.

The Cap Rate provides a standardized way to compare properties and assess their relative value. For example, if you are considering two properties with similar market values but different Cap Rates, the one with the higher Cap Rate could indicate a potentially more profitable investment.

Moreover, the Cap Rate helps investors determine the risk associated with a particular investment. Generally, properties with higher Cap Rates are considered riskier because they may require more extensive renovations or have a higher likelihood of vacancies. On the other hand, properties with lower Cap Rates are often considered safer investments due to their stable income streams.

By analyzing the Cap Rate, investors can make more informed decisions and ensure they are maximizing their returns. It allows them to evaluate potential investment opportunities and assess the financial viability of a property.

High Cap Rate or Low Cap Rate?

You might be wondering upfront: is a high cap rate better than a low cap rate? Well, the answer depends on whether you own a deal or want to purchase one and fix it up.

Let me begin by outlining the big picture first, and then we’ll delve into the details. I’ll cover this topic in four steps:

- Calculating the Cap Rate: This is A simple explanation of the cap rate, including the mathematical equation and one of its alternative expressions.

- Dynamics of the Cap Rate: understanding how the math works in motion.

- How the Cap Rate is used: applying the math in practical scenarios.

- The different perspectives are based on how one would use the cap rate: considering who you are in the deal and what you care about.

Calculating the Cap Rate

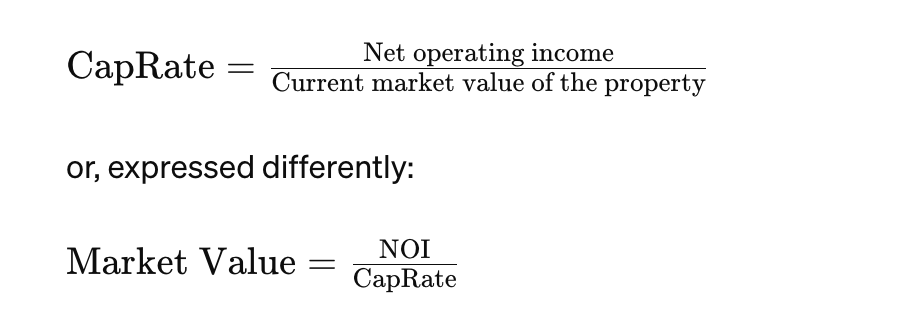

To calculate the Cap Rate, you need to know the property’s net operating income (NOI) and its current market value. The formula for calculating the Cap Rate is as follows:

Cap Rate = Net Operating Income (NOI) / Current Market Value

The net operating income (NOI) is calculated by subtracting the operating expenses from the property’s gross income. Operating expenses include property taxes, insurance, maintenance costs, and property management fees. The current market value is the estimated worth of the property based on recent sales and comparable properties in the area.

Let’s say you are considering a property with a gross income of $100,000 and operating expenses of $30,000. The net operating income (NOI) would be $70,000. If the property’s current market value is $1,000,000, the Cap Rate would be calculated as follows:

Cap Rate = $70,000 / $1,000,000 = 0.07 or 7%

In this example, the Cap Rate is 7%, indicating that the property has the potential to generate a 7% return on investment based on its current income and market value.

The primary equation for determining the cap rate is straightforward:

For example, if a property valued at $1 million produces an annual NOI of $80k, it could be measured as an 8% cap rate.

But simplicity is rare. There’s always an “it depends” waiting around the corner.

When solving multi-variable equations, it’s best to understand each variable separately to grasp its impact on the whole equation. Once understood, simplifying and solving can help determine if a prospective deal is right. Answers vary among investors, depending on their investment goals, risk tolerance, and comfort with the deal’s management.

Here’s a list of crucial variables to consider:

(1) Current Market Value: This can vary due to factors such as asset class, location, condition, amenities, safety, surrounding market conditions, and potential economic prospects. The Current Market Value of a property varies due to

- its “asset class”

- its location

- geo, noise, …

- its condition

- its amenities

- its ease of access

- its age and type of construction

- its safety

- fenced in, security cameras, etc.

- its surrounding market and submarkets

- its ability to stay (near) fully leased

- its surrounding competition and their rent rates

- its prospective economic potential (or past)

- and other “it depends”

So basically, a property is evaluated relative to the market around it – much like a single-family residence is valued relative to its neighborhood.

(2) NOI: This can be influenced by increasing gross income and decreasing expenses, a topic worthy of its own discussion.

3) One’s Position in the Deal: Whether as a passive investor, sponsor, key principal, or banker.

(4) Stage of Acquisition: Whether looking for a deal, in pre-closing stages, involved in a new acquisition, managing a stabilized property, or involved in selling, 1031 exchanging, or refinancing.

2. Dynamics of Cap Rate – The Math in Motion

Let’s start with the straightforward implications of the equation:

a) If a property’s market value (MV) increases while NOI remains constant, its Cap Rate (CR) decreases.

b) If MV remains constant while NOI increases, then CR increases.

c) If MV decreases while NOI remains constant, then CR increases.

d) If both MV and NOI change, specific details are required to determine whether CR increases or decreases.

Now, let’s consider a less obvious application of cap rate:

Cap rate can be used to assess risk in a deal. For instance, when a bank evaluates lending funds to a sponsor, they can adjust the Loan to Value (LTV) rate they are willing to offer. Additionally, they can determine their own cap rate for the specific property under consideration. If the property carries more risk, they will set a slightly higher cap rate, effectively lowering the overall value of the property since they view the Net Operating Income (NOI) as a key factor in their calculation. Conversely, if the property is in a prime location with significant potential for growth, they may lower their cap rate, thereby increasing the property’s value based on the current NOI. Does this seem perplexing? Let’s explore some examples in the next section.

3. How is Cap Rate Used – The Math Applied

Consider this scenario: if a property under consideration for purchase is located in a desirable area, such as a newly revitalized city center, a loan officer might recognize its potential for increased value. Consequently, they may be inclined to lend the sponsor more funds while maintaining the Loan to Value (LTV) ratio.

By utilizing the equation MV = NOI/CR, and assuming a fixed Net Operating Income (NOI) for an existing property being sold to the sponsor, lowering the cap rate on a fixed NOI implies a higher market value (MV). This suggests that the amount one can borrow increases. However, it also acknowledges the inherent risk in the deal while hoping for potential upside. As the saying goes, “higher risk, higher potential gains” (along with higher potential losses).

Another example to illustrate this concept: suppose you intend to sell the property. Having a lower Cap Rate at the time of sale may result in receiving more money when it is sold, assuming all other factors remain constant. If this seems counterintuitive, consider a few examples:

- if your NOI is 100,000 and the CR is 10%, then the valuation of the property is 1,000,000

- if your NOI is 100,000 and the CR is 8%, then the valuation of the property is 1,250,000

In translation, a lower Cap Rate (CR) signifies a higher relative value of a property in the eyes of lenders. This could be influenced by various factors such as current market conditions, neighborhood desirability, and growth potential. However, from the sponsor’s perspective, a higher cap rate during operations indicates receiving a higher cash flow compared to the current market value of the property. This might seem perplexing at first glance. Just remember the equation and apply it according to your perspective and situation in a deal.

4. The Different Perspectives Are Based on How One Would Use the Cap Rate – The “Who are you?” and “Why would you care?”

So, what are your goals?

Suppose you, as a group of sponsors and passive investors, intend to undertake a value play, which involves acquiring a depreciated property and improving it to increase the Net Operating Income (NOI). In that case, your approach will focus on comparing the current Cap Rate (CR) of the property to that of similar properties in the surrounding market. For instance, if neighboring properties with an NOI of $100,000 have a cap rate of 8% (implying a market value of $1.25 million), and the property you’re evaluating, once renovated, would fall into the same class and is offered for $1 million with an NOI of $100,000 (resulting in a 10% CR), and you anticipate increasing the NOI by 10% to $110,000, then, assuming an 8% CR in the market post-renovation, the property’s value would be approximately $1.375 million.

If your Loan to Value (LTV) on the purchase was 75% (with a downpayment of $250,000 plus $100,000 in rehab expenses, totaling $375,000 as a group of investors), the deal could likely be refinanced in about 3 years at 80% LTV, providing nearly $350,000 in equity back to you as investors. This translates to a 93% return of capital in 3 years, or roughly a 31% Internal Rate of Return (IRR). Moreover, you still retain ownership of the property and continue to receive quarterly distributions.

If you received an 8% Cash on Cash (CoC) return in the 3rd year (or $8,800 annually), with almost all your money back except $25,000, your annualized return on the remaining capital in the deal would be 35%. Even after refinancing, while monthly mortgage expenses may increase and distributions may slightly decrease, a $7,000 distribution on $25,000 represents a 28% return on your remaining capital in the deal.

Additionally, there are tax advantages due to depreciation and mortgage pay-down from rent collections, and you don’t have to pay taxes on the $350,000 obtained through refinancing because it’s technically “loan” money (although the tenants are still covering the mortgage). However, value plays typically don’t offer substantial CoC distributions during the rehab phase.

If you’re simply seeking a yield play, the calculations remain the same, but the increase in NOI and decrease in CR may not be as pronounced. Yield plays prioritize providing cash flow to investors and usually involve less risk. They cater to those seeking regular income, such as retirees.

For individuals evaluating a property’s performance, particularly loan officers at banks, the focus is primarily on managing risk. This website isn’t designed to teach banking intricacies, but it’s important to understand that banks aim to mitigate risk while still turning a profit.

Final Thoughts

Understanding the Cap Rate is crucial for real estate investors. It provides a standardized metric for evaluating the financial viability of a property, comparing different properties, and assessing their relative value.

In addition to understanding the Cap Rate, we encourage our clients to consider the following thoughts before investing:

- Recognize your role in the acquisition process—whether you’re a potential passive investor, a sponsor, or another party involved.

- Determine your purpose in evaluating the investment—whether you’re assessing performance, potential, or other factors.

- Consider other aspects of the deal to gain a comprehensive understanding, such as performas and overall Internal Rate of Return (IRR).

- If necessary, consult with others who are also evaluating similar opportunities, but remember to respect confidentiality, especially regarding Private Placement Memorandums (PPMs). If you have questions, don’t hesitate to ask your sponsor.

Lastly: South Silver Group and its affiliates are not licensed financial advisors or consultants. The information provided on this platform is for educational and informational purposes only. We do not offer personalized financial advice or recommendations for specific investment decisions. Any actions taken based on the information provided are at your own risk. It is recommended to consult with a licensed financial professional or advisor before making any investment decisions.

Please reach out to us with any questions.

CONTACTS

View Other Articles

- /

Understanding Soft Commitment Investments

A Brief History of Marinas and Their Current Market

Defining A Typical Marina Investment

Marina Investments Opportunities Worth Exploring

Minimum Investment Requirements

Real Estate Glossary of Terms

What is A Cap Rate?

Why Are There Different Types of Shares in a Deal?

How to Start Investing in Real Estate and Grow Your Wealth